01

Portfolio-aware research

Run simple single-asset tests or expand into multi-asset, multi-strategy portfolios with capital allocation, exposure tracking, consolidated metrics, and attribution.

Research. Validate. Deploy.

A quantitative trading framework built for disciplined strategy research, portfolio-aware validation, and explicit live deployment handoffs.

Features

Run simple single-asset tests or expand into multi-asset, multi-strategy portfolios with capital allocation, exposure tracking, consolidated metrics, and attribution.

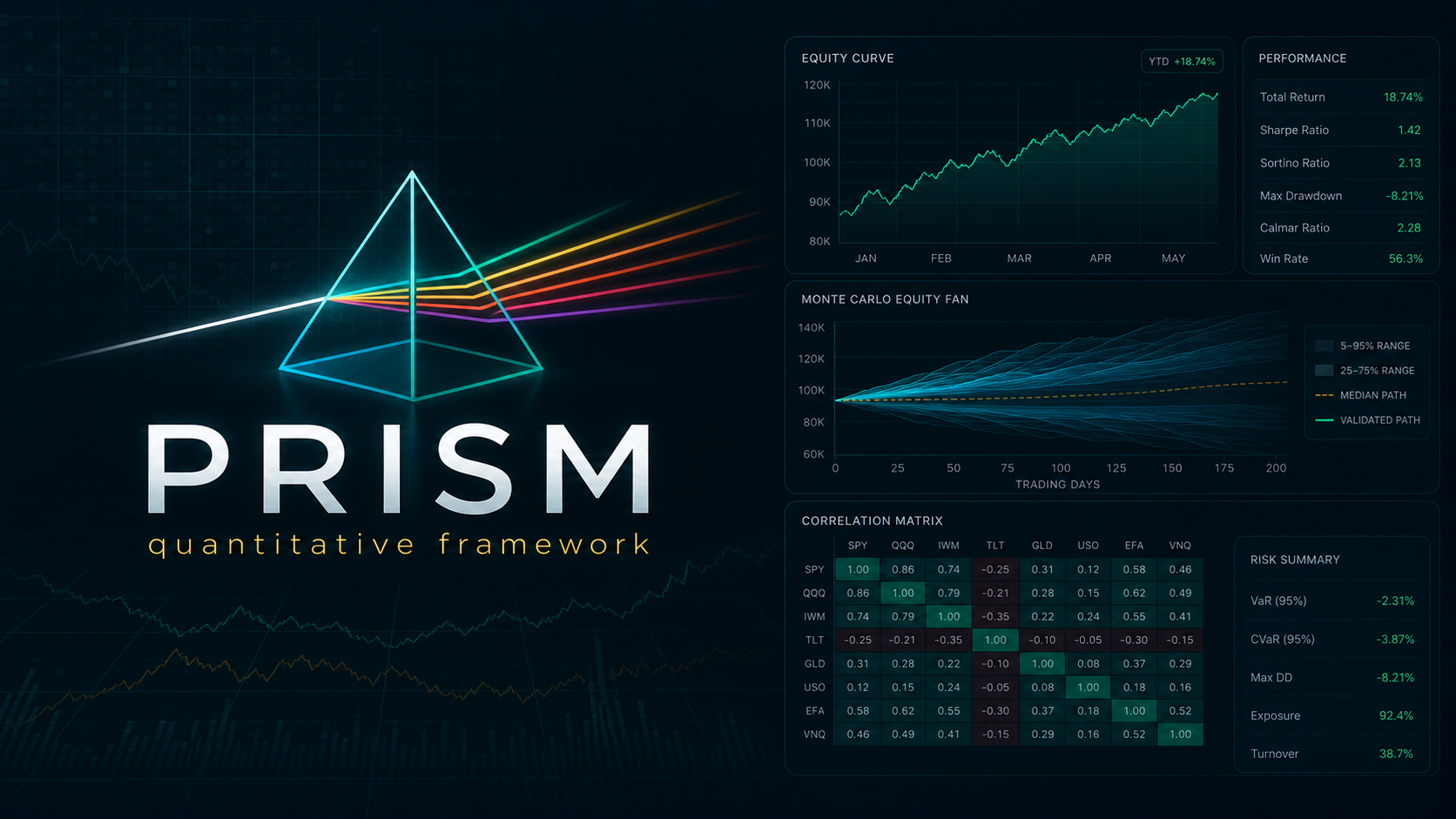

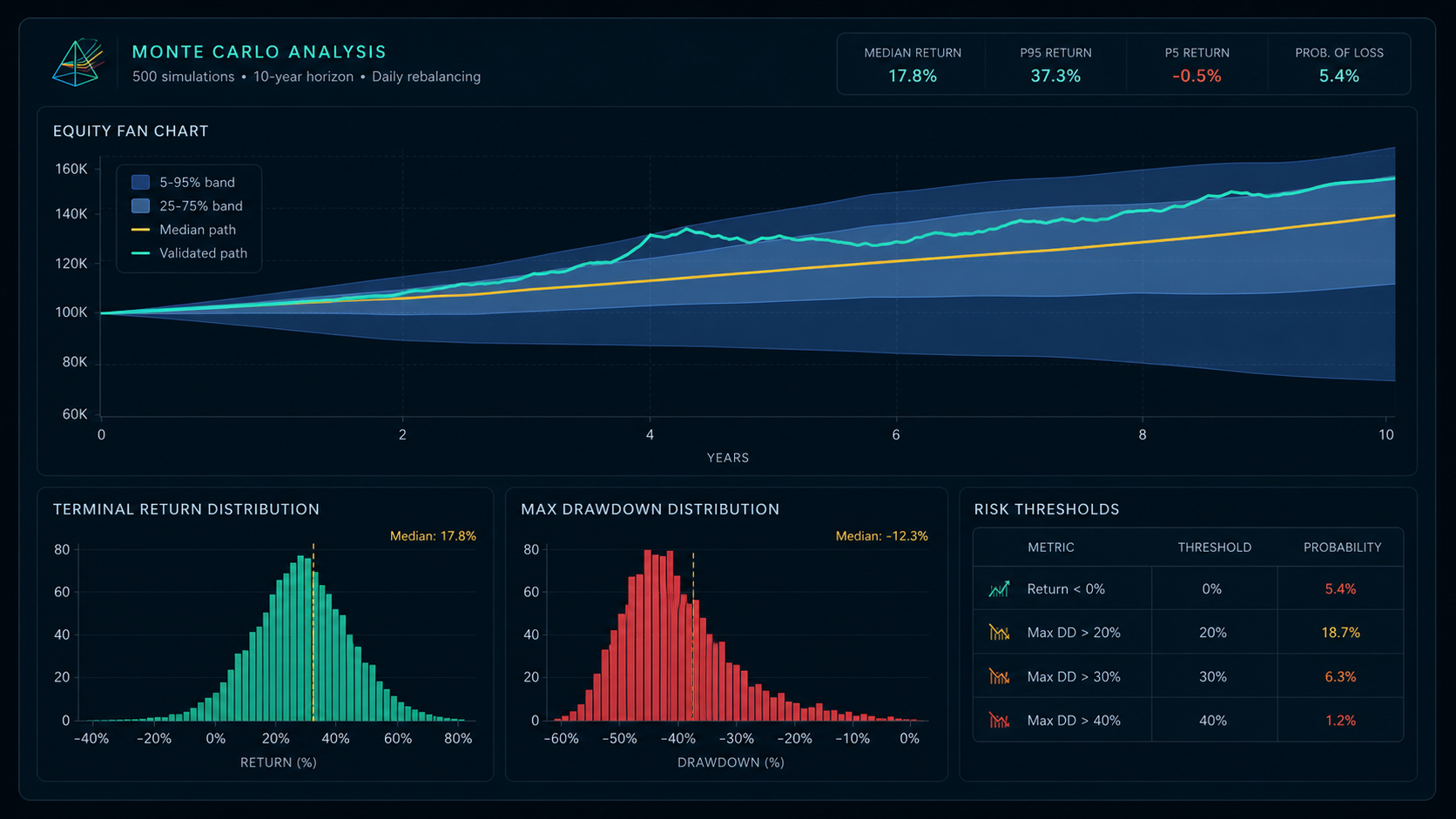

Move from baseline backtests into parameter optimization, walk-forward validation, Monte Carlo stress testing, paper testing, and deployment review.

Use the reference event-driven engine for correctness, then accelerate compatible workloads through vectorized execution modes for broad research studies.

Ingest market data through a provider registry, normalize bars into a canonical store, track acquisition attempts, and reuse universes across download and research flows.

Preserve stable run identifiers, strategy versions, parameter sets, data scope, chart snapshots, reports, and downstream artifacts in a connected research record.

Promote validated candidates intentionally, emit webhook payloads to a live engine, and monitor positions, orders, PnL, signals, fills, and errors from one operator view.

Roadmap

The roadmap follows the framework design docs: strengthen the data foundation, deepen validation, then scale into live portfolio operation and faster research loops.

Build a durable acquisition catalog with auto-ingest, provider-aware provenance, freshness summaries, scheduled task visibility, and reusable universes that drive downloads, backtests, and portfolio studies.

Add an asset reference backbone, enrichment pipelines, provider-separated detail panes, saved filters, preview counts, and one-click handoff from screener results into universes and research workflows.

Advance parameter optimization with robust-region detection, clustering, formal candidate promotion, richer explorer compare modes, walk-forward validation, and Monte Carlo stress testing as cataloged artifacts.

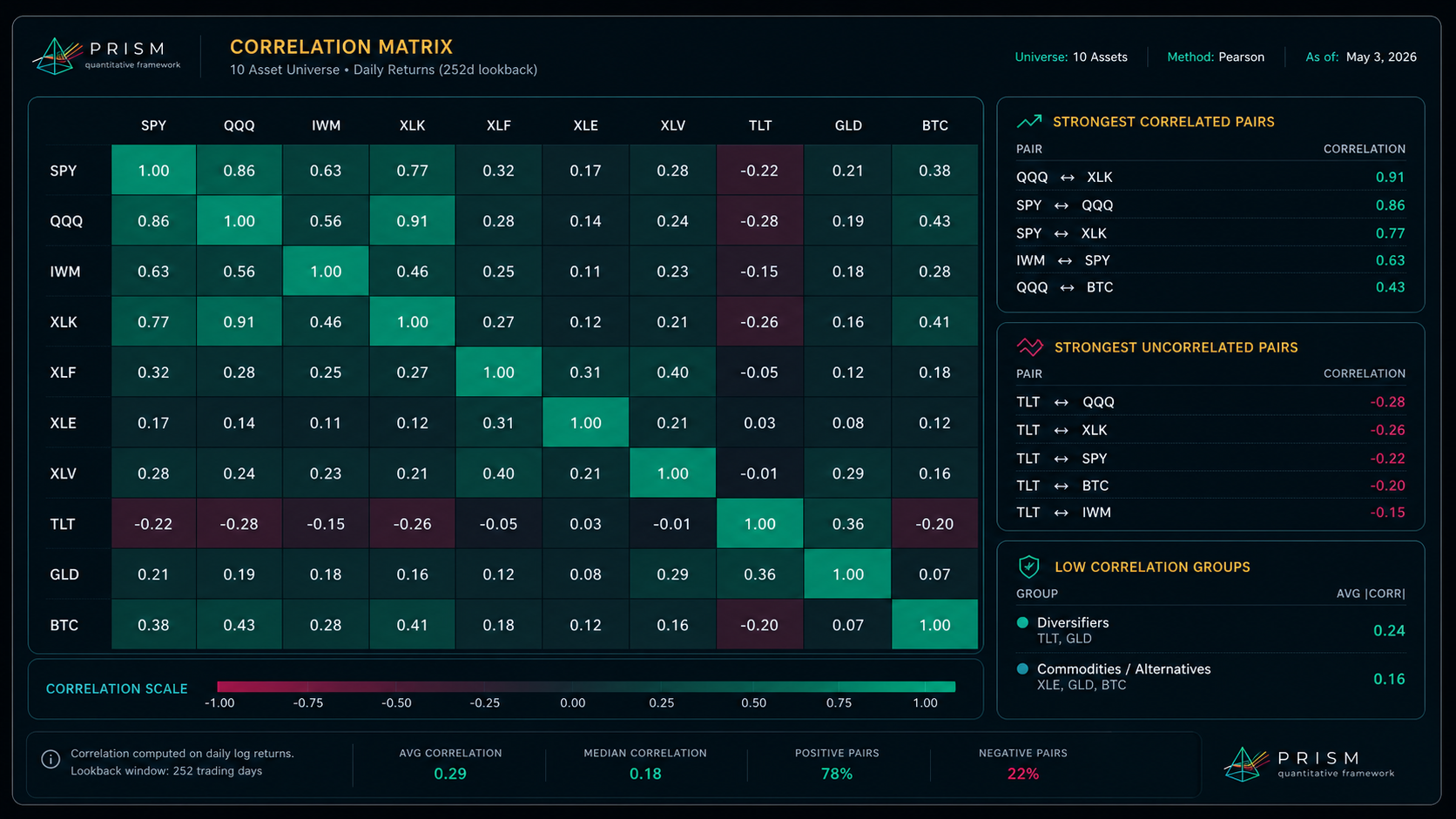

Extend scoring and reporting around portfolio aggregation, correlation checks, attribution, strategy and asset exposure, annual-volatility sizing, and explicit margin and gross-exposure controls.

Promote validated or manual deployments into a live workflow with lineage-rich webhooks, Interactive Brokers first live data, signal journaling, live metrics, and pause, resume, and stop controls.

Use ChartSnapshot artifacts with Magellan-ready rendering, add a ticker-driven market workspace, and phase in vectorized execution with parity checks, resumable jobs, and faster batch scheduling.

Pricing

Start on the waitlist, then choose the research depth that matches how close you are to deployment.

Waitlist

For traders who want launch updates and early product direction.

Researcher

For solo quants validating strategies before taking them live.

Operator

For active traders who need portfolio research and deployment monitoring.

Sign Up

Join the early access list and help shape which workflow ships first: research, portfolio construction, validation, or live monitoring.